[ad_1]

The monetary world handed a milestone in 2024: for the primary time, the property managed by passive funding methods within the U.S. exceeded these below active administration, marking the height of a decade-long shift towards indexing at the price of lively managers’ market share.

The S&P Annual Survey of Property from final 12 months reveals a staggering $11 trillion now listed to the S&P 500, and rightly so.1 The SPIVA 2023 scorecard highlights a telling trend: over the past decade, a mere fraction, less than 13%, of U.S. large-cap funds have managed to surpass the S&P 500’s efficiency.2

But, the explosive progress of passive investing presents a paradox for traders. Every announcement of constituent modifications by the S&P 500 propels cash managers right into a whirlwind of exercise, adjusting their holdings to align with the index’s. Nevertheless, this flurry of trades usually prompts short-term value fluctuations, doubtlessly skewing future returns.

Decoding the Rebalancing Act

Behind the S&P 500, the Normal & Poor’s Committee meticulously curates the index utilizing a course of that entails a cautious consideration of things like market capitalization, liquidity and sector illustration.3

Rebalancing the index, however, extends beyond administrative upkeep, profoundly affecting the stocks being welcomed or bid farewell. As mutual funds and ETFs that track the S&P 500 recalibrate their holdings to include new additions, a surge in demand often follows, temporarily influencing stock prices.

Similarly, index drops result in selling pressure for stocks that are shunned by the committee.

This phenomenon is known as the “index effect,” and sets the stage for significant trading activity, often by arbitrageurs looking to capitalize on these short-term fluctuations.

As more traders try to capitalize on this index effect between the announcement and effective date, the actual movement of the stock once added or removed from the index can deviate from what we would expect, especially in the long run.

The new dynamic flips the traditional index effect narrative: stocks chosen by the committee to be added usually already have lofty valuations, plus they now take pleasure in a pre-inclusion rally, solely to then face post-addition sluggishness. In the meantime, shares chosen to be dropped, normally after short-term headwinds, are hit by an additional wave of promoting, after which they regularly rebound from their lowered ranges and turn into winners but once more.

Latest Modifications and Their Affect

To get a greater sense of what’s taking place across the announcement and efficient change dates, let’s check out two current excessive profile rebalances.

First, the rebalance on December 21, 2020. On November 16, S&P announced that Tesla would be added to the S&P 500, however solely introduced what firm can be dropped later.4 From November 16 to December 18, Tesla had a complete return of over 70%, in comparison with the S&P 500’s 3%.

A couple of weeks later, S&P introduced that Residence Funding and Administration Co (AIV) was the corporate that may be dropped.5

Figure 1: Post-Rebalance Performance—An Example from the 2020 S&P 500 Index Rebalance

In the six months after the rebalance, TSLA had underperformed the S&P 500 by over 23% and AIV had outperformed by over 47%.6

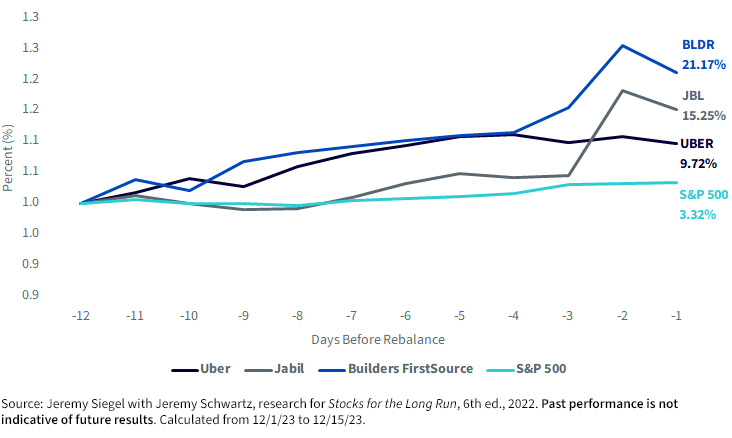

More recently, there was a rebalance on December 18, 2023.

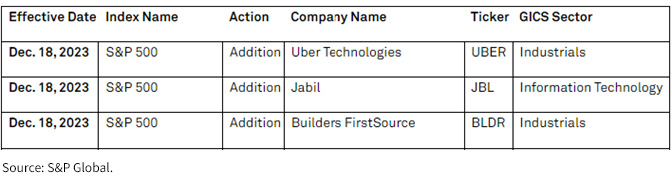

Determine 2: S&P 500 Proclaims the Additions for the 2023 Rebalance

Taking a look at this rebalance date, we see that every one three of the proposed additions outperformed the S&P 500 within the two weeks between the announcement date and the efficient date. Uber outperformed by over 6%, Jabil by nearly 12%, and Builders First Supply by nearly 18%.7

Figure 3: Performance of the S&P 500 Index Additions—the 2023 Rebalance Example

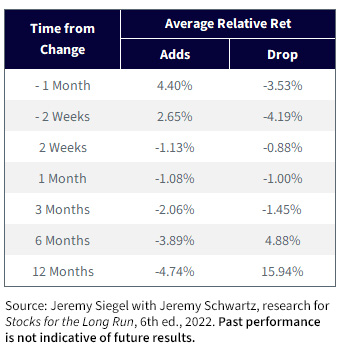

Expanding the Lens: A Five-Year Review

To get a better sense of this effect, we collected all the changes that occurred in the S&P 500 since 2019. This accounts for five years of constituent changes, specifically only looking at stocks that underwent changes where companies were chosen by the committee.

Figure 4: Looking at Historical S&P 500 Index Rebalances, Comparing Performance of Additions to Performance of Deletions Leading into and then After the Event

Adds: Specifically, stocks poised for inclusion in the S&P 500 tended to outshine the broader index by about 2.6% in the two-week run-up to their addition. However, once officially added, these stocks often fell short of the index and on average they underperformed by 4.7% over the next 12 months.

Drops: Conversely, companies on the verge of removal experienced an initial downturn, selling off before their actual exclusion. Yet, once removed, these stocks frequently started to recover, outpacing the index by nearly 5% on average in the following six months and by almost 16% over the next 12 months.

This pattern we see around the rebalance of indexes underscores how the explosion of passive investing and index changes can have long lasting impacts for adds/drops to the index.

We believe that investors and market strategists should consider these trends when navigating index rebalancing events, as they can have significant implications for investment strategies.

Stay tuned for a forthcoming in-depth research piece that will explore these index changes in greater detail, providing a more comprehensive understanding of their impact on the market and a deeper understanding of how this effect intertwines with popular value and low volatility narratives.

1 Source: “S&P Dow Jones Indices Annual Survey of Assets,” S&P Global, https://www.spglobal.com/spdji/en/documents/index-news-and-announcements/spdji-indexed-asset-survey-2022.pdf

2 Supply: “SPIVA® U.S. Scorecard,” S&P World, https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2023.pdf

3 Supply: “S&P U.S. Indices Methodology,” S&P World, https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-us-indices.pdf

4 Supply: “Tesla Set to Be a part of S&P 500,” S&P World, https://www.spglobal.com/spdji/en/documents/indexnews/announcements/20201116-1258362/1258362_tdec215addconsult.pdf

5 Supply: Brian Scheid, “Residence Funding & Administration Dropped from S&P 500 to Make Means for Tesla,” S&P World, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/apartment-investment-management-dropped-from-s-p-500-to-make-way-for-tesla-61715093

6 Supply: “Uber Applied sciences, Jabil and Builders FirstSource Set to Be a part of S&P 500; Others to Be a part of S&P MidCap 400 and S&P SmallCap 600,” S&P World, https://www.spglobal.com/spdji/en/documents/indexnews/announcements/20231201-1467851/1467851_dec2023shuf.pdf

7 Supply: Jeremy Siegel with Jeremy Schwartz, analysis for Shares for the Lengthy Run, sixth ed., 2022. Previous efficiency just isn’t indicative of future outcomes. Calculated from 12/1/23 to 12/15/23.

[ad_2]

Source link